A New Dawn of Health Care

November 13, 2024

The Turnaround of a Global Epidemic?

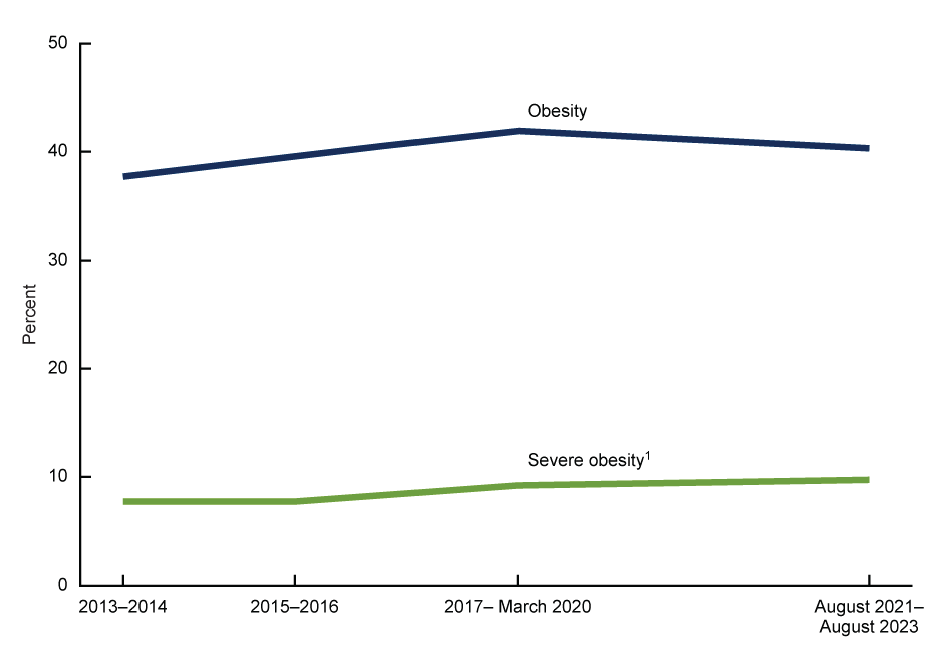

In September, the CDC reported that 40.3% (~134 million) of adults in the United States were considered obese (defined as a body-mass index (BMI) reading above 30).1 These statistics have risen steadily in the U.S. and across the globe. In the U.S., obesity rates increased by 39% from 2000-2018, and severe obesity was up 95% in that same period. Worldwide, obesity has doubled since 1990, and adolescent obesity has quadrupled.

But recent data has shown a leveling-off of obesity rates in the U.S. For the first time in a decade, the obesity rate has not increased between sample periods, likely due to new medical treatments and technological advancements. From 2013-2014 to 2021-2023, the age-adjusted prevalence of obesity in adults did not significantly change, but severe obesity rates rose from 7.7% to 9.7% (~25 million to ~32.5 million).2

A “Healthier” World

The first GLP-1 agonist was approved by the food and drug administration (FDA) in 2005. GLP-1 stands for glucagon-like peptide-1; a type of medication that helps manage blood sugar (glucose) levels in people with type 2 diabetes.4 The medication mimics the release of insulin which lowers glucose (sugar) in the blood and blocks glucagon (a hormone produced by the body to raise blood sugar levels) from entering the bloodstream. As a result, extra insulin lowers blood sugar levels, and the medication slows the movement of food from the stomach into the small intestine, reducing overall appetite and food intake levels.

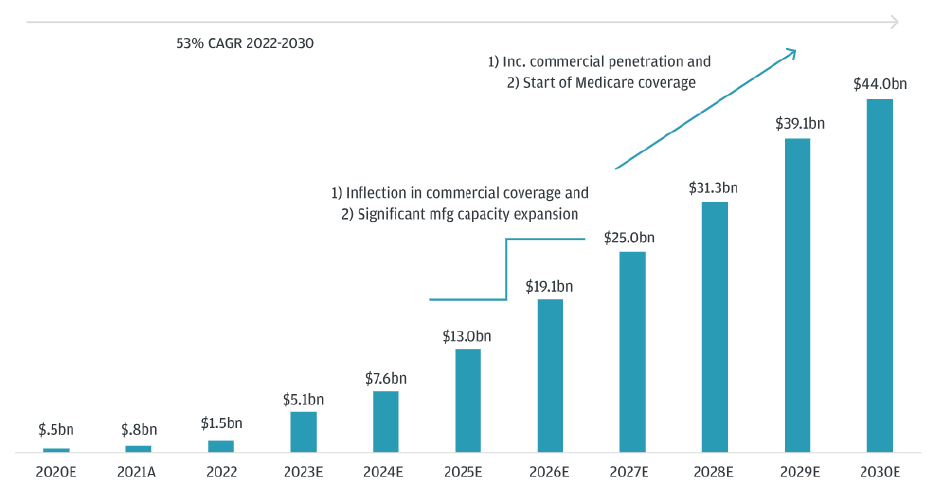

Today, 10-12% of type 2 diabetic patients in the U.S. use GLP-1s. By 2030, estimates show this number will rise to 35%, and that total GLP-1 users in the U.S. could reach 30 million – approximately 9% of the population.5 With this, the total addressable market for GLP-1 drugs could exceed $100 billion by 2030.

Who is Leading this Charge?

Two companies are leading the market in GLP-1 and type 2 diabetes/weight-loss products: U.S.-based Eli Lilly and Company (LLY) and Denmark’s Novo Nordisk (NOVO.B-DK). Both companies offer a variety of diabetes and weight-loss-focused products.

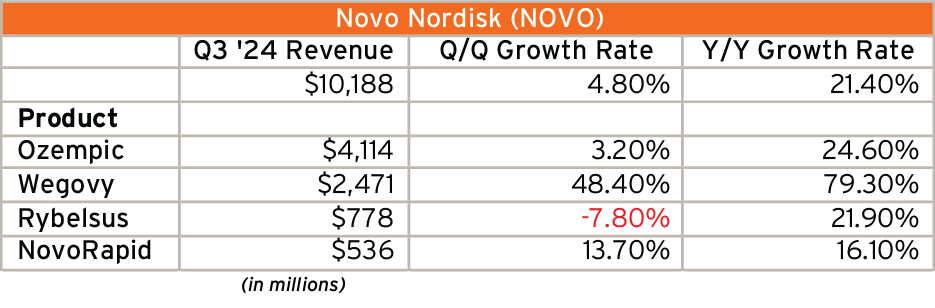

Ozempic, NOVO’s type 2 diabetes GLP-1 medication, was approved by the FDA in 2017. In 2023, Ozempic revenues topped 95 million Danish Krone ($13.5 billion USD), up from 59 billion DKK ($8.4 billion) in 2022. NOVO’s obesity-marketed product, Wegovy, grew revenues from 6.1 billion DDK in 2022 to 31.1 billion DDK in 2023 ($856 million to $4.4 billion) - over a 400% growth rate in just a year.

But the U.S.-based LLY is closing the gap on NOVO. LLY’s GLP-1 treatment for type 2 diabetes is Trulicity, approved by the FDA in the fall of 2014. Trulicity has also been shown to reduce the risk of heart attack and stroke in adults with type 2 diabetes. In 2023, Trulicity revenues were $7.1 billion, down from $7.4 billion in 2022. This was mostly due to LLY releasing a new drug, Mounjaro, which was FDA-approved in the spring of 2022. Mounjaro is more effective at weight loss and blood sugar control than Trulicity; Mounjaro revenues grew from nearly $500 million in 2022 to $5.2 billion in 2023. As of the third quarter, Mounjaro revenues were $3.1 billion, up 41% y/y, and Trulicity revenues were $1.3 billion, down 22% y/y. Both of these products are not FDA-approved weight-loss medications, they are solely prescribed for type 2 diabetes.

The fall of 2023 brought a new product to LLY’s offerings: Zepbound. Unlike Mounjaro and Trulicity, Zepbound is a weight-loss approved medication for obesity. Zepbound has been shown to reduce body weight by 22.5% on average, the most across all available medications on the market.7 Zepbound revenues grew from $175 in Q4 2023 to $1.2 billion in Q3 2024.

Looking Ahead For LLY

LLY declined by over 6% following the release of its third quarter results. As similar to other portfolio adjustments we have made in the past, we viewed the sell-off as taking advantage of the dislocation and negative sentiment to buy a best-in-class business. In the third quarter, LLY grew total revenues by 42%. Excluding its top two growing products (Mounjaro and Zepbound), revenues still rose 17% y/y, showing the company’s diverse portfolio of treatments. Revenues grew in the U.S. market by 46%, driven by a 35% increase in volume and 11% increase in price.

Recently, the industry has been negatively affected following Trump’s victory and the likelihood of Robert F. Kennedy Jr. and lobbyists’ involvement in the industry, possibly putting downward pressure on the use and further adoption of these products. But we see GLP-1s, and weight-loss treatments more broadly, to be multi-year themes. These treatments are leading to an average weight reduction of 15-25%, and studies have shown that patients quickly gain back weight if they pause their usage. Furthermore, Morningstar projects LLY and NOVO to retain nearly 70% of the total market by 2031, given their first-mover advantage and grip on the industry. We believe as insurance companies cover a greater portion of the cost, leading to lower costs for consumers, broader adoption is likely to follow.

Stephanie Link’s TV Schedule:

Investment Solutions is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC, member FINRA and SIPC. Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC. This is not an offer to buy or sell securities. No investment process is free of risk, and there is no guarantee that the investment process or the investment opportunities referenced herein will be profitable. Past performance is neither indicative nor a guarantee of future results. The investment opportunities referenced herein may not be suitable for all investors. All data or other information referenced herein is from sources believed to be reliable. Any opinions, news, research, analyses, prices, or other data or information contained in this presentation is provided as general market commentary and does not constitute investment advice. Investment Solutions and Hightower Advisors, LLC or any of its affiliates make no representations or warranties express or implied as to the accuracy or completeness of the information or for statements or errors or omissions, or results obtained from the use of this information. Investment Solutions and Hightower Advisors, LLC assume no liability for any action made or taken in reliance on or relating in any way to this information. The information is provided as of the date referenced in the document. Such data and other information are subject to change without notice. This document was created for informational purposes only; the opinions expressed herein are solely those of the author(s) and do not represent those of Hightower Advisors, LLC, or any of its affiliates.

1Source: CDC. As of September 2024.

2Source: CDC. As of September 2024.

3Source: CDC. As of September 2024.

4Source: Cleveland Clinic. As of July 3, 2023.

5Source: JP Morgan Research. As of November 29, 2023.

6Source: JP Morgan Research. As of November 29, 2023.

7Source: NBC News. As of November 8, 2023.

8Source: Bloomberg. As of November 11, 2024

200 W Madison, 25th Floor

Chicago, IL 60606

(312) 962-3800

hightoweradvisors.com